The Economic Impact of Flooding, Part 3:

The Legacy of Super Storm Sandy

This is the third part of our series on the economic impact of flooding. You can read the first part of the series on the aftermath of Hurricanes Laura and Delta here and the second part on recent floods in Mississippi here.

From the Mississippi floodplain and to the Atlantic coast, homeowners have been facing more intense disasters more frequently in the past decade. For many who have lost their homes in the wake of a natural disaster, the question of whether it’s worth it to rebuild in the same location or move on isn’t easy. This has been particularly difficult for those whose attention has been torn between a prolonged recovery effort and the desire to look to the future.

How can you plan where you’ll be in ten years if you’re not confident that the rising coastline won’t endanger your beachside home again next hurricane season?

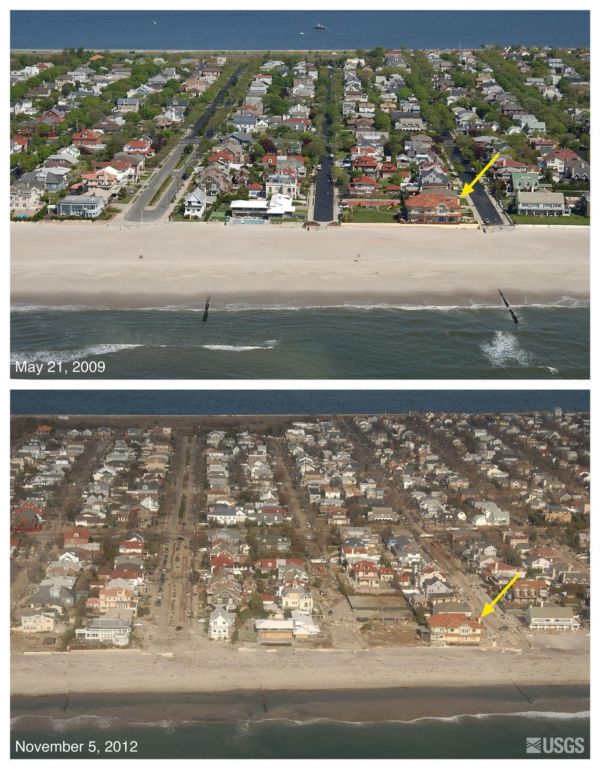

This question was particularly pressing for those impacted by Super Storm Sandy in 2012. The storm killed at least over a hundred people and caused $19 billion worth of damage and an estimated $32.8 billion in restoration costs across New York state.

Nearly nine years later, let’s look at the economic impact of flooding in the wake of Sandy and the question of rebuilding.

The Economic Impact of Flooding: Super Storm Sandy by the Numbers

The direct impact Sandy on five boroughs was enormous, and it was initially difficult to quantify on the homeowner-level. According to estimates released by the Mayor’s Office in 2013, the direct private losses in New York City totaled $8.6 billion, of which $4.8 billion were uninsured.

The Mayor’s office also reported that over 23,000 businesses and nonprofits were located in areas flooded by Sandy, which accounted for the employment of about 245,000 people. They noted that “nearly 95 percent of these impacted enterprises were small- and medium-sized (employing 50 or fewer people), with many concentrated in the retail and service sectors.”

A number of major enterprises in Lower Manhattan were also impacted by the storm surge, as well as manufacturers with coastal locations across several boroughs, including Brooklyn, Queens, and Staten Island. But much of the worst damage to individual New Yorkers happened where they lived in the outer boroughs. For many of these folks, the recovery took years.

This is also true on the municipal level: a 2019 report from Comptroller Scott Stringer found that “only 54 percent of $14.7 billion in federal aid set aside for city repairs and resiliency has actually gone toward those efforts.”

Why? Stringer’s office cited federal bureaucracy, but it’s difficult to explain this seven-year delay in resiliency spending.

Fortunately for homeowners, the question of speed to recovery has less to do with major federal funding allocations and more to do with their own preparedness and local resources. In the years since Sandy, we’ve seen firsthand that insurance agents play a key role in facilitating flood assistance for property owners.

If you’d like to know more about how better flood claim management can bolster a community’s economic recovery, visit our agent resource library.

The Long-Term Economic Impact of Sandy Is Difficult to Quantify

The short answer is that Super Storm Sandy is just one in a string of disasters to impact the city over the past decade, including the COVID-19 pandemic. The longer answer is that New York City – like many American metropoli – is behind on resiliency planning. We can begin to look at how Sandy shaped these efforts in New York by looking at Staten Island.

One year after Sandy made landfall, the Governor’s Office of Storm Recovery (GOSR) had already acquired 299 homes in the borough at a cost of $122 million, but this step toward managed retreat was isolated to neighborhoods that suffered the most damage in Staten Island: Oakwood Beach, Ocean Breeze, and Graham Beach. These neighborhoods quickly saw the majority of their structures demolished by the city and a swift return to nature, as Curbed documented in 2013.

But this strategy hasn’t been applied to all waterfront neighborhoods in New York City, many of which are expected to become increasingly vulnerable to flooding as the climate continues to change. Instead, the city has given its attention to a project called Rebuild By Design, which is an impressive project that was funded by $920 million of disaster recovery funding from HUD.

While these innovative projects are exciting, many say they don’t go far enough to protect homeowners in any borough. Many homeowners didn’t go anywhere after the storm hit in 2012, and while they may have taken some flood mitigation measures in rebuilding, the fact of their location leaves them vulnerable to future flooding.

The Legacy of Super Storm Sandy Is Better Flood Awareness

Here in the midst of the COVID-19 pandemic, after a year of exodus for homeowners and renters in York City, it’s difficult to look back and say exactly what impact Sandy’s damage still has today. But its legacy is trifold:

- Local, city, and state governments in this area continue to face the question of climate resilience with the memory of Sandy’s aftermath still fresh in their minds.

- Public interest and community investment in flood mitigation efforts didn’t just surge after the storm; it remains high on residents’ priority lists.

- Homeowners in coastal communities are more acutely aware of their flood risk and the importance of having adequate flood coverage.

Those who had flood insurance may never have filed a flood claim before Sandy, and others who didn’t think it was worth it to purchase coverage were convinced of the importance of having adequate flood insurance overnight.

While in some areas that were impacted by Sandy, it may be difficult for borrowers to get a mortgage today, the coastlines the super storm hit hardest weren’t abandoned ten years later. It continues to be important for communities, insurers, and homeowners to think ahead to the next storm and prepare to respond and recover, should the next hurricane season bring more flooding to their shores.

The Real Question of Rebuilding: Where to Go to Avoid Future Floods

According to the 2013 New York City Panel on Climate Change (NPCC) report, mid-range projections for sea level rise in the 2050s are 11-24 inches and the high estimate is 31 inches. With this near-term forecast, the question of where to go if they don’t choose to rebuild is challenging for individual homeowners.

And homeowners who do wish to abandon the coasts will have to do their homework. The risk of inland flooding is increasing as water rises along the coasts, and those who are looking to avoid future water damage will need to take their heightened awareness of flood risk with them, wherever they move.

The only thing homeowners can do is to get to know their flood risk, wherever they live, and insurance agents can play an important role in this ongoing education process. If the legacy of Sandy is better local awareness for New Yorkers, it should be a stronger commitment to homeowner education on the part of insurance companies. Contact us today for more information about training resources.

Blog Articles